Student Loan Repayment: 2026 Income-Driven Plans for Recent Graduates

Navigating Student Loan Repayment 2026: A Comprehensive Guide for Recent US Graduates

The transition from college life to the professional world is often accompanied by a significant financial reality check: student loan debt. For recent US graduates, understanding and effectively managing this debt is paramount to building a stable financial future. As we look towards 2026, the landscape of student loan repayment is continuously evolving, with new policies and adjustments to existing programs designed to offer relief and manageable pathways. This comprehensive guide will delve into the critical aspects of income-driven repayment plans, focusing on the latest updates and strategies for recent graduates to optimize their student loan repayment 2026.

The burden of student loan debt in the United States remains a pressing issue, impacting millions of individuals. While the prospect of paying back tens of thousands of dollars can feel daunting, a wealth of resources and programs are available to help. The key lies in understanding these options and proactively choosing the best path for your unique financial situation. This article aims to demystify the complexities of student loan repayment for those who have recently earned their degrees, offering practical advice and a forward-looking perspective on what to expect in 2026.

The Current State of Student Loan Debt for Recent Graduates

Before diving into repayment strategies, it’s essential to acknowledge the context. Recent graduates are entering a dynamic job market, often with varying levels of income and financial commitments. The average student loan debt continues to be substantial, making informed repayment decisions more crucial than ever. Many graduates find themselves balancing entry-level salaries with rent, living expenses, and the looming presence of student loan bills. This financial juggling act underscores the importance of flexible repayment options.

Understanding your specific loan types (federal vs. private) and their associated interest rates is the first step. Federal loans typically offer more borrower protections and flexible repayment plans, including income-driven options, which will be our primary focus. Private loans, while sometimes offering competitive rates, generally lack the same level of flexibility and borrower-friendly provisions. For the purposes of student loan repayment 2026, federal loan programs will be the most impactful for the majority of recent graduates.

The economic climate also plays a significant role. Inflation, interest rates, and employment trends can all influence a graduate’s ability to make consistent loan payments. Therefore, having a repayment plan that can adapt to these external factors is invaluable. Income-driven repayment (IDR) plans are specifically designed with this flexibility in mind, making them a cornerstone of effective debt management for many.

Understanding Income-Driven Repayment (IDR) Plans in 2026

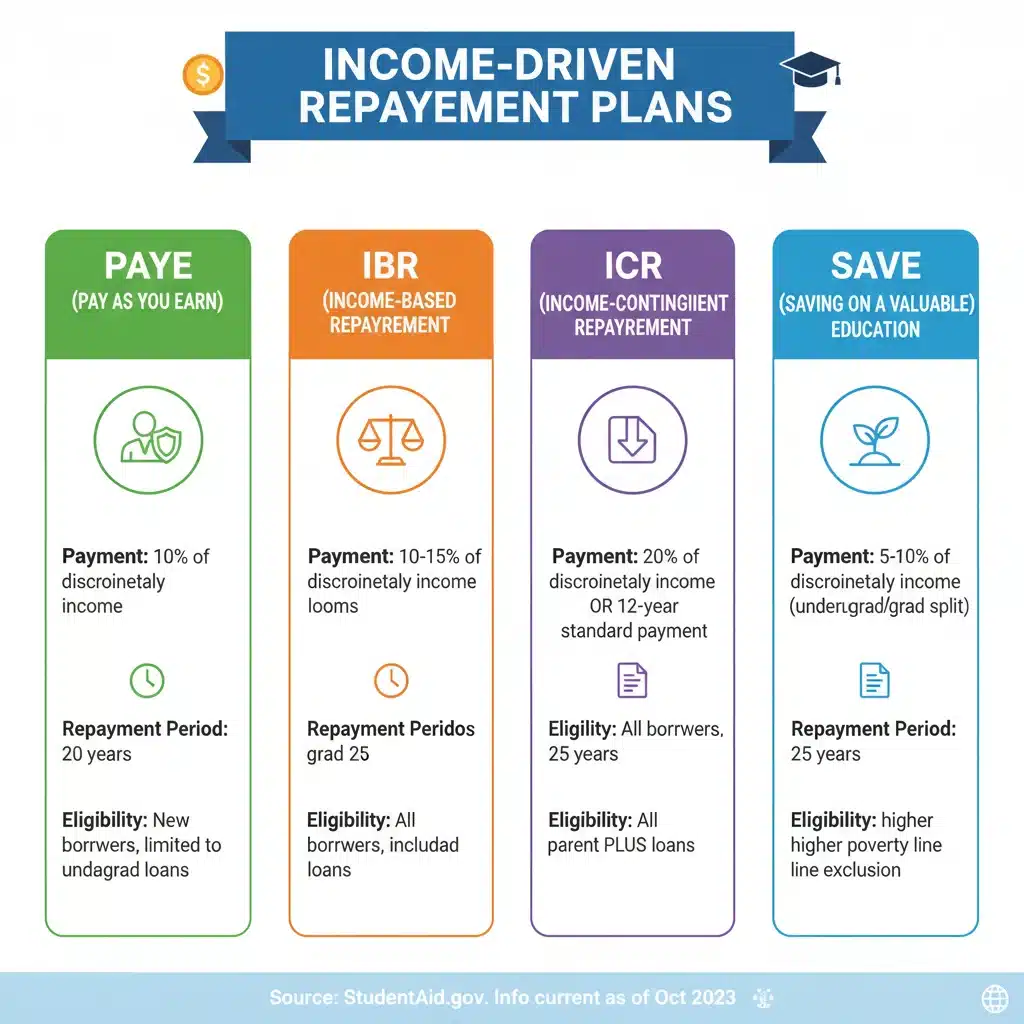

Income-Driven Repayment (IDR) plans are federal programs designed to make student loan payments more manageable by capping them at a percentage of your discretionary income. As of 2026, these plans continue to be a lifeline for many borrowers, especially those with lower incomes relative to their debt burden. The primary IDR plans include:

- Saving on a Valuable Education (SAVE) Plan: This is the newest and arguably most beneficial IDR plan for many recent graduates, especially post-July 2024.

- Pay As You Earn (PAYE) Repayment Plan: Offers payments capped at 10% of discretionary income.

- Income-Based Repayment (IBR) Plan: Payments are typically 10% or 15% of discretionary income, depending on when you took out your loans.

- Income-Contingent Repayment (ICR) Plan: Payments are the lesser of 20% of discretionary income or what you’d pay on a fixed 12-year plan, adjusted for income.

The core principle behind all IDR plans is to ensure that your monthly loan payments are affordable, preventing default and providing a pathway to eventual loan forgiveness. This flexibility is crucial for recent graduates who may be in entry-level positions with lower salaries but still carry significant educational debt. Understanding which plan best suits your financial situation is key to optimizing your student loan repayment 2026 strategy.

The SAVE Plan: A Game-Changer for Student Loan Repayment 2026

The Saving on a Valuable Education (SAVE) Plan, which fully rolled out in July 2024, is poised to be the most impactful IDR plan for many recent graduates in 2026. It replaces the Revised Pay As You Earn (REPAYE) Plan and offers significant improvements, particularly for those with lower incomes.

Key Features of the SAVE Plan:

- Lower Monthly Payments: For undergraduate loans, monthly payments are reduced from 10% to 5% of discretionary income. For graduate loans, the payment rate remains at 10%, and for borrowers with both undergraduate and graduate loans, it will be a weighted average.

- Increased Income Exemption: The amount of income protected from repayment calculations has increased from 150% to 225% of the federal poverty line. This means more of your income is considered non-discretionary, leading to lower monthly payments. For a single borrower, this could mean an income of around $33,000 (as of 2024 poverty guidelines) would result in a $0 monthly payment.

- Interest Subsidy: Perhaps the most significant benefit: if your monthly payment doesn’t cover the accrued monthly interest, the government covers the remaining interest. This prevents your loan balance from growing due to unpaid interest, a common issue with other IDR plans. This feature alone can save borrowers thousands of dollars over the life of their loans and prevent the dreaded ‘negative amortization.’

- Shorter Forgiveness Timelines for Smaller Balances: Borrowers who originally borrowed $12,000 or less could see their remaining loan balance forgiven after just 10 years of payments. For every additional $1,000 borrowed above $12,000, one additional year of payments is added, up to a maximum of 20 or 25 years.

- Spousal Income Exclusion: Unlike REPAYE, if you’re married and file separately, your spouse’s income is no longer included in your payment calculation under SAVE. This is a huge benefit for many married couples.

For recent graduates, the SAVE Plan offers an unprecedented level of affordability and protection against ballooning interest. It’s a critical component of any student loan repayment 2026 strategy, especially for those in the early stages of their careers with entry-level salaries.

Comparing IDR Plans: Which One is Right for You in 2026?

While the SAVE Plan offers compelling advantages, it’s still important to understand the nuances of all IDR plans to determine the best fit. Your specific loan types, income level, family size, and future career prospects will all influence this decision.

Here’s a brief comparison to help recent graduates evaluate their options for student loan repayment 2026:

- SAVE vs. PAYE: For most new borrowers with only undergraduate loans, SAVE will likely offer lower payments and the interest subsidy benefit, making it superior to PAYE. However, PAYE still exists for those who qualified for it previously and might prefer its specific terms, particularly if they have graduate loans and a higher income. The maximum repayment period for PAYE is 20 years, while SAVE is 20-25 years.

- SAVE vs. IBR: IBR payments are generally 10% or 15% of discretionary income, with a maximum repayment period of 20 or 25 years. SAVE’s 5% for undergraduate loans and the interest subsidy typically make it a more attractive option, especially for those seeking to minimize their monthly outflow and prevent interest capitalization.

- SAVE vs. ICR: ICR is generally the least generous IDR plan, with payments capped at 20% of discretionary income. Unless you have specific loan types only eligible for ICR (like Parent PLUS loans consolidated into a Direct Consolidation Loan), SAVE will almost always offer more favorable terms.

It’s crucial to use the Federal Student Aid Loan Simulator to compare payments under different plans based on your specific financial information. This tool is invaluable for making an informed decision about your student loan repayment 2026 strategy.

Eligibility and Application for IDR Plans

To enroll in an IDR plan, including SAVE, you generally need to have federal student loans. Most Direct Loans and FFEL Program loans are eligible. Parent PLUS loans, however, require consolidation into a Direct Consolidation Loan before they can be repaid under an IDR plan (specifically ICR, though the consolidated loan can then be consolidated again to become eligible for SAVE). Perkins Loans are also eligible after consolidation.

Application Process:

- Gather Financial Information: You’ll need your most recent tax return or other documentation of your current income (e.g., pay stubs).

- Determine Family Size: This impacts your discretionary income calculation.

- Apply Online: The easiest way to apply is through StudentAid.gov. You can typically complete the application in about 10-20 minutes.

- Annual Recertification: Once enrolled, you’ll need to recertify your income and family size annually. This is crucial for maintaining your affordable payments and preventing your loans from reverting to a standard repayment plan with potentially higher payments. Missing your recertification deadline can lead to interest capitalization and increased monthly payments. Mark your calendar and set reminders for this critical annual task to ensure continuous optimization of your student loan repayment 2026.

Recent graduates should aim to apply for an IDR plan as soon as their grace period ends, or even before, to ensure they start repayment on the most favorable terms possible. Don’t wait until you’re struggling to make payments; proactive enrollment can prevent financial stress and potential default.

Other Important Repayment Strategies for 2026

While IDR plans are a cornerstone, they are not the only strategy. A holistic approach to student loan repayment 2026 involves several other considerations:

1. Public Service Loan Forgiveness (PSLF)

For graduates working in public service (government, non-profit organizations), PSLF offers forgiveness of the remaining balance on Direct Loans after 120 qualifying monthly payments (10 years) made under a qualifying repayment plan, typically an IDR plan. This program can be incredibly beneficial, effectively erasing significant debt for those committed to public service careers. Ensure you’re working for a qualifying employer and submitting the annual PSLF Employer Certification Form.

2. Employer Student Loan Assistance Programs

A growing number of employers are offering student loan assistance as a benefit. This can range from direct contributions to your loan principal to financial wellness programs. When evaluating job offers, inquire about such benefits, as they can significantly reduce your overall debt burden. This trend is expected to continue and even expand into 2026, making it a valuable consideration for recent graduates entering the workforce.

3. Refinancing Private Student Loans

If you have private student loans, refinancing them with a lower interest rate can save you a substantial amount of money over the life of the loan. This is particularly advantageous if your credit score has improved since you first took out the loans or if interest rates have dropped. However, be cautious: refinancing federal loans into private loans means losing access to federal benefits like IDR plans, forbearance, deferment, and potential forgiveness programs. This option is generally only recommended for private loans.

4. Making Extra Payments When Possible

Even if you’re on an IDR plan, any extra payments you can make will directly reduce your principal balance, leading to less interest paid over time and potentially a shorter repayment period. If you receive a bonus, a tax refund, or find yourself with extra cash, consider directing a portion towards your student loans. Always specify that extra payments should be applied to the principal of the loan with the highest interest rate first.

5. Building an Emergency Fund

While paying down debt is important, having an emergency fund is critical. It provides a financial safety net for unexpected expenses like medical emergencies or job loss, preventing you from going into further debt or missing loan payments. Aim for at least 3-6 months of living expenses in an easily accessible savings account.

6. Understanding Deferment and Forbearance

In times of financial hardship, deferment and forbearance can temporarily pause your loan payments. While these options offer relief, interest may still accrue, potentially increasing your total loan cost. They should be used as a last resort and understood thoroughly before opting in. However, knowing they exist provides a crucial safety net for managing unexpected life events during your student loan repayment 2026 journey.

Common Pitfalls to Avoid in Student Loan Repayment 2026

Even with the best intentions, recent graduates can fall into common traps that hinder their repayment progress. Being aware of these can help you steer clear:

- Ignoring Your Loans: The absolute worst thing you can do is ignore your student loans. This can lead to default, severe credit damage, wage garnishment, and even loss of professional licenses. Always communicate with your loan servicer if you’re struggling.

- Missing Annual Recertification: As mentioned, forgetting to recertify your income and family size for IDR plans can lead to higher payments and interest capitalization. Set multiple reminders!

- Not Understanding Your Loan Types: Mixing up federal and private loans, or not knowing the specific terms of each, can lead to poor decisions. Federal loans offer protections that private loans do not.

- Falling for Scams: Be wary of companies promising quick fixes or guaranteed loan forgiveness for a fee. Most student loan assistance can be found for free through official channels like StudentAid.gov or your loan servicer.

- Overpaying on Private Loans When Federal Options Exist: If you have both federal and private loans, prioritize understanding federal options first due to their flexibility. Don’t rush to pay off private loans if it means sacrificing essential federal protections without a clear strategy.

- Not Budgeting Effectively: Without a clear understanding of your income and expenses, managing student loans becomes significantly harder. Create and stick to a budget that allocates funds for loan payments, savings, and living expenses.

Looking Ahead: The Future of Student Loan Repayment Beyond 2026

The landscape of student loan repayment is constantly evolving due to legislative changes, economic shifts, and ongoing advocacy efforts. While we focus on student loan repayment 2026, it’s worth noting that further adjustments to federal programs are always possible.

The long-term goal of many policymakers and advocates is to create a more equitable and affordable higher education financing system. This could include further simplifications of IDR plans, expanded eligibility for forgiveness programs, or even broader reforms to tuition costs. Staying informed through official government sources like StudentAid.gov is crucial for understanding any future changes that might impact your repayment strategy.

For recent graduates, the best approach is to remain adaptable and proactive. Regularly review your loan portfolio, stay updated on policy changes, and re-evaluate your repayment plan as your financial situation or life circumstances change. What works for you today might not be the optimal solution in a few years, especially with the dynamism evident in student loan repayment 2026 and beyond.

Conclusion: Empowering Your Student Loan Repayment 2026 Journey

Navigating student loan repayment as a recent US graduate in 2026 can seem overwhelming, but with the right knowledge and strategy, it is entirely manageable. The introduction and full implementation of the SAVE Plan, alongside existing IDR options, offer powerful tools to make your monthly payments affordable and prevent your debt from spiraling out of control. By understanding your loan types, choosing the most appropriate repayment plan, and staying proactive with annual recertifications and financial planning, you can take control of your financial future.

Remember to leverage official resources like StudentAid.gov, communicate with your loan servicer, and consider seeking advice from accredited financial counselors if you need personalized guidance. Your journey of student loan repayment 2026 is a marathon, not a sprint. With careful planning and consistent effort, you can successfully manage your student debt and move towards achieving your broader financial goals.