Mortgage Rates 2026: Secure Your 30-Year Fixed Rate Below 6.5%

The housing market is a dynamic entity, constantly influenced by a myriad of economic factors, geopolitical events, and shifting consumer sentiment. For prospective homebuyers and current homeowners looking to refinance, understanding the trajectory of mortgage rates 2026 is paramount. As we approach the mid-2020s, the question on everyone’s mind is: what will mortgage rates look like, and is it possible to secure a 30-year fixed rate below 6.5% before the year concludes? This comprehensive guide delves into expert predictions, economic indicators, and strategic advice to help you navigate the evolving landscape of mortgage financing.

Securing a favorable mortgage rate can translate into significant savings over the life of a loan, directly impacting monthly payments and overall financial well-being. The prospect of a 30-year fixed rate below 6.5% is an attractive one, offering stability and predictability in an often-unpredictable market. This article will explore the forces that drive mortgage rates, provide a detailed forecast for 2026, and equip you with actionable strategies to position yourself for the best possible outcome.

Understanding the Drivers of Mortgage Rates

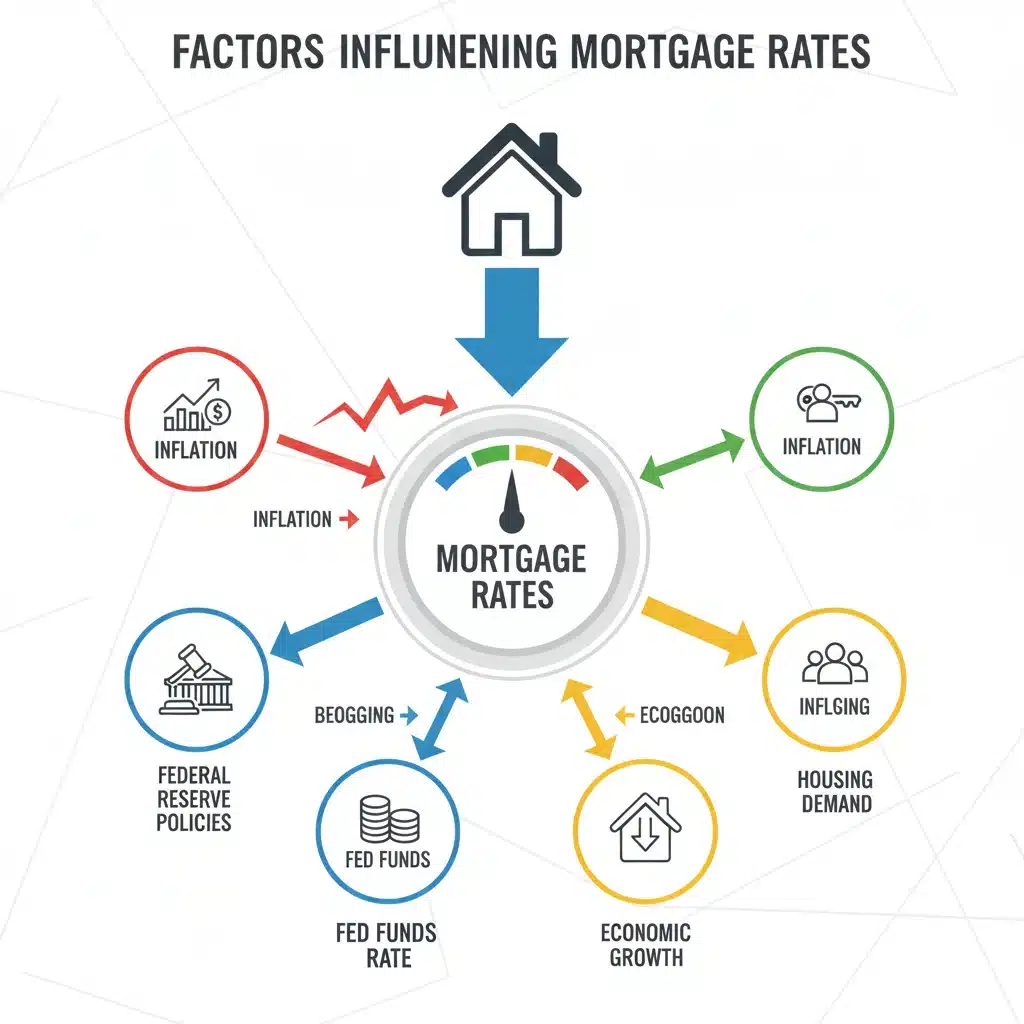

Before we can accurately project mortgage rates 2026, it’s crucial to understand the fundamental economic principles and market forces that dictate their movement. Mortgage rates are not set in a vacuum; they are a complex interplay of several key factors.

The Federal Reserve and Monetary Policy

The Federal Reserve (the Fed) plays a pivotal role in influencing interest rates across the economy, including mortgage rates. While the Fed does not directly set mortgage rates, its actions, particularly regarding the federal funds rate, have a significant indirect impact. When the Fed raises the federal funds rate, it generally makes borrowing more expensive for banks, which then pass these higher costs on to consumers in the form of higher interest rates for various loans, including mortgages. Conversely, when the Fed lowers rates, it tends to stimulate lending and economic activity, often leading to lower mortgage rates.

Inflation: The Silent Rate Driver

Inflation is another critical factor. Lenders consider the erosion of purchasing power over time due to inflation. If inflation is high, lenders demand higher interest rates to compensate for the decreased value of the money they will be repaid in the future. Therefore, controlling inflation is often a primary objective of the Fed, and their success or failure in doing so directly impacts mortgage rate trends. A sustained period of low and stable inflation could create an environment conducive to lower mortgage rates 2026.

Economic Growth and Employment

A robust economy with strong job growth typically leads to higher demand for housing, which can put upward pressure on home prices and, indirectly, on mortgage rates. Lenders perceive a strong economy as less risky, but increased demand for credit can still push rates higher. Conversely, an economic slowdown or recession often sees a dip in mortgage rates as the Fed may cut rates to stimulate the economy, and demand for loans might soften.

The Bond Market: A Direct Link

Perhaps the most direct influence on fixed mortgage rates comes from the bond market, specifically the yield on the 10-year Treasury note. Mortgage-backed securities (MBS), which are bundles of mortgages sold to investors, compete with Treasury bonds for investor attention. When Treasury yields rise, MBS yields must also rise to remain competitive, leading to higher mortgage rates. Therefore, keeping an eye on the 10-year Treasury yield provides a good real-time indicator of where mortgage rates are headed.

Global Economic Conditions

In an increasingly interconnected world, global economic conditions, such as international trade, geopolitical stability, and economic growth in major global powers, can also indirectly affect U.S. mortgage rates. For instance, global economic uncertainty can lead investors to seek the relative safety of U.S. Treasury bonds, driving down their yields and potentially leading to lower mortgage rates.

Forecasting Mortgage Rates 2026: Expert Insights

Predicting future mortgage rates is an inherently challenging endeavor, as it relies on forecasts of numerous economic variables. However, by analyzing current trends, historical data, and expert consensus, we can build a reasonable outlook for mortgage rates 2026.

Current Economic Landscape and Trajectory

As we move towards 2026, many economists anticipate a period of normalization following recent economic volatility. The expectation is that inflation will continue to moderate, albeit perhaps not reaching the Fed’s target of 2% immediately. This gradual cooling of inflation could allow the Federal Reserve to adopt a more accommodative monetary policy, potentially leading to rate cuts.

Consensus on 2026 Rate Movement

While specific numbers vary, a general consensus among many financial institutions and housing market analysts suggests that mortgage rates 2026 could see a modest decline from their recent peaks. The possibility of a 30-year fixed rate falling below 6.5% before year-end hinges on several factors:

- Continued Disinflation: If inflation trends downward consistently, the Fed will have more room to cut the federal funds rate, which should translate to lower mortgage rates.

- Stable Economic Growth: A ‘soft landing’ for the economy, where inflation cools without a significant recession, would be ideal. This scenario would support a healthy housing market with potentially lower rates.

- Bond Market Stability: As mentioned, the 10-year Treasury yield is key. If investor confidence in the economy remains strong, and inflation fears subside, bond yields could stabilize or even decrease, pulling mortgage rates down.

Some optimistic forecasts suggest that if economic conditions align perfectly, we could see average 30-year fixed rates dip into the high 5% to low 6% range by the latter half of 2026. However, it’s crucial to remember that these are projections, and actual outcomes can differ.

Potential Headwinds and Risks

Despite the optimistic outlook, several factors could prevent mortgage rates 2026 from dropping below the 6.5% threshold or even push them higher:

- Resurgent Inflation: Unexpected spikes in energy prices, supply chain disruptions, or robust wage growth could reignite inflationary pressures, forcing the Fed to keep rates higher for longer.

- Geopolitical Instability: Global conflicts or significant geopolitical events can create economic uncertainty, leading to increased demand for safe-haven assets like U.S. Treasury bonds, which could initially push yields down but then cause volatility.

- Stronger-Than-Expected Economic Growth: While generally positive, an overheating economy could lead the Fed to delay rate cuts or even consider further hikes to contain inflation.

Therefore, while the target of a 30-year fixed rate below 6.5% in 2026 is plausible, it is not a certainty. Homebuyers and refinancers should remain agile and informed.

Strategies to Secure a 30-Year Fixed Rate Below 6.5% Before Year-End 2026

Even with an uncertain future, there are proactive steps you can take to increase your chances of securing a competitive 30-year fixed rate, potentially below 6.5%, in 2026. Preparation and strategic planning are key.

1. Improve Your Credit Score

Your credit score is one of the most significant determinants of the interest rate you’ll be offered. Lenders use your credit score to assess your creditworthiness and the likelihood of you repaying the loan. A higher credit score (generally 760 or above) signals less risk to lenders, often qualifying you for the lowest available rates. Focus on:

- Paying bills on time.

- Reducing outstanding debt.

- Avoiding opening new credit accounts unnecessarily.

- Regularly checking your credit report for errors.

2. Save for a Larger Down Payment

A larger down payment reduces the amount you need to borrow, which can decrease your loan-to-value (LTV) ratio. A lower LTV ratio often translates to a lower interest rate, as it reduces the lender’s risk. Aim for at least 20% down to avoid private mortgage insurance (PMI) and qualify for better rates.

3. Shop Around for Lenders

Do not settle for the first offer you receive. Mortgage rates can vary significantly between different lenders, even for the same borrower profile. Contact multiple banks, credit unions, and mortgage brokers to compare rates, fees, and terms. A difference of even a quarter of a percentage point can save you tens of thousands of dollars over the life of a 30-year mortgage.

4. Consider a Mortgage Rate Lock

If you find a favorable rate while actively searching, inquire about a rate lock. A rate lock guarantees your interest rate for a specific period (e.g., 30, 45, or 60 days) while your loan application is being processed. This protects you if rates rise before your loan closes. Be aware of any fees associated with rate locks and their duration.

5. Understand Different Mortgage Products

While a 30-year fixed rate is popular for its stability, it’s worth understanding other mortgage products. Adjustable-Rate Mortgages (ARMs), for example, might offer lower initial rates, but their rates can fluctuate after an introductory period. For those planning to move or refinance again within a few years, an ARM might be considered, but for long-term stability, the 30-year fixed remains the gold standard, especially if you can secure a rate below 6.5%.

6. Monitor Economic News and Fed Announcements

Stay informed about economic indicators, inflation reports, and Federal Reserve meetings. These announcements often precede shifts in mortgage rates. Being aware of these trends can help you time your mortgage application or refinancing decision more effectively, aligning it with periods of potential rate decreases.

The Role of Refinancing in 2026

For current homeowners, 2026 could present a prime opportunity for refinancing. If you secured a mortgage at a higher interest rate in previous years, a dip in mortgage rates 2026, particularly below 6.5%, could make refinancing financially advantageous. Refinancing can lower your monthly payments, reduce the total interest paid over the loan term, or even allow you to tap into your home equity.

When to Consider Refinancing

- Lower Interest Rates: The primary reason to refinance is to secure a lower interest rate than your current one.

- Shorter Loan Term: You might refinance from a 30-year to a 15-year mortgage to pay off your home faster, though this typically comes with higher monthly payments.

- Switching from ARM to Fixed: If you have an ARM and want to lock in a stable rate, especially if rates are projected to rise, refinancing into a fixed-rate mortgage is a smart move.

- Cash-Out Refinance: This allows you to borrow more than you owe on your current mortgage and take the difference in cash, often used for home improvements, debt consolidation, or other large expenses.

Before refinancing, calculate the break-even point – the time it takes for the savings from your lower interest rate to offset the closing costs of the new loan. If you plan to stay in your home beyond this point, refinancing is likely a good decision.

Impact on the Housing Market

The trajectory of mortgage rates 2026 will undoubtedly influence the broader housing market. If rates do indeed fall below 6.5%, we could see a resurgence in buyer demand. Lower borrowing costs make homeownership more affordable, potentially attracting more first-time buyers and those who were previously priced out of the market.

Increased Affordability

Even a small decrease in interest rates can significantly impact affordability. For example, a homeowner with a $400,000 mortgage at 7% pays approximately $2,661 per month (principal and interest). If that rate drops to 6%, the payment falls to around $2,398, a savings of over $260 per month. This increased purchasing power can stimulate demand.

Potential for Price Appreciation

Increased demand, coupled with potentially still-limited housing supply in many areas, could lead to continued, albeit perhaps more moderate, home price appreciation. However, a significant influx of buyers could also lead to bidding wars in competitive markets, pushing prices up more rapidly. The balance between supply and demand will be crucial.

Builder Confidence

Lower mortgage rates also tend to boost builder confidence. With more buyers able to afford homes, developers are more likely to invest in new construction, which is vital for addressing the ongoing housing shortage. This could lead to a more balanced market in the long run.

The Importance of Professional Guidance

Navigating the complexities of mortgage financing, especially with an eye on future rates, is best done with the help of experienced professionals. Mortgage brokers, loan officers, and financial advisors can provide personalized advice based on your specific financial situation and goals.

Mortgage Brokers vs. Direct Lenders

- Mortgage Brokers: They work with multiple lenders and can shop around on your behalf to find the best rates and terms. They can be particularly useful if you have a unique financial situation or want to compare a wide range of options.

- Direct Lenders (Banks, Credit Unions): These institutions lend their own money and can sometimes offer competitive rates, especially if you have an existing relationship with them.

Regardless of whom you choose, ensure they are reputable, transparent about fees, and willing to clearly explain all aspects of the loan process. Ask for pre-approvals to understand what you can afford and to strengthen your offer when purchasing a home.

Conclusion: Positioning Yourself for Success in 2026

The outlook for mortgage rates 2026 is cautiously optimistic, with a plausible scenario where 30-year fixed rates could dip below 6.5% before the year’s end. This projection is underpinned by expectations of moderating inflation and a potentially more accommodative stance from the Federal Reserve. However, economic forecasts are subject to change, and various internal and external factors could influence the actual trajectory of rates.

For prospective homebuyers and existing homeowners considering a refinance, the key to success lies in preparation and vigilance. By focusing on improving your credit score, saving for a substantial down payment, diligently shopping for lenders, and staying informed about economic trends, you can significantly enhance your chances of securing a highly competitive mortgage rate. Engaging with financial professionals will further empower you to make informed decisions tailored to your unique circumstances.

As 2026 unfolds, the housing market will continue to evolve. Those who are well-prepared and proactive will be best positioned to capitalize on favorable rate environments, ensuring financial stability and achieving their homeownership goals. Keep a close watch on the economic indicators, and be ready to act when the market conditions align to secure your desired 30-year fixed rate.