Protect Your 2026 Retirement: Inflation Hedge Strategies Explained

Protect Your 2026 Retirement: Inflation Hedge Strategies Explained

The specter of inflation looms large over retirement planning, particularly as we look towards 2026 and beyond. For many, retirement savings represent years of diligent work and careful financial management. However, the purchasing power of those hard-earned dollars can diminish significantly if not adequately protected against rising costs. Understanding and implementing effective strategies to hedge against inflation is not merely a recommendation; it’s a critical imperative for securing your financial future. This comprehensive guide will delve into the impact of inflation on your 2026 retirement savings and, more importantly, equip you with actionable strategies, including the crucial concept of a 4% hedge, to safeguard your wealth and ensure a comfortable retirement.

The Silent Thief: How Inflation Erodes Your Retirement Savings

Inflation is often referred to as the ‘silent thief’ because it gradually erodes the purchasing power of money over time. While a 2% or 3% annual inflation rate might seem negligible in the short term, its cumulative effect over decades can be devastating for retirement planning. Imagine you’ve meticulously saved enough to live comfortably on $50,000 a year in today’s dollars. If inflation averages 3% annually, in 20 years, you’ll need approximately $90,305 to maintain the same standard of living. This means your current savings, if not growing at a rate higher than inflation, will buy significantly less in the future. For those targeting retirement in 2026 or soon after, this reality is even more pressing, as the time horizon for corrective action is shorter.

The impact of inflation extends beyond just the cost of everyday goods. It affects healthcare expenses, housing costs, transportation, and leisure activities – essentially every aspect of your post-working life. A fixed income stream, such as a traditional pension or annuities that aren’t inflation-adjusted, becomes less valuable with each passing year. This is why a proactive approach to inflation protection is paramount. Without it, your carefully constructed retirement nest egg could fall far short of your needs, forcing difficult choices or a reduced quality of life.

Understanding the historical trends of inflation and projecting potential future scenarios is a fundamental step in building a robust retirement plan. While predicting exact future inflation rates is impossible, assuming a conservative average of 2-4% is a prudent approach for long-term financial modeling. This assumption allows you to build a buffer into your investment strategy, ensuring that your savings are not just growing, but growing faster than the cost of living.

The 4% Hedge: A Strategic Approach to Retirement Inflation Hedge

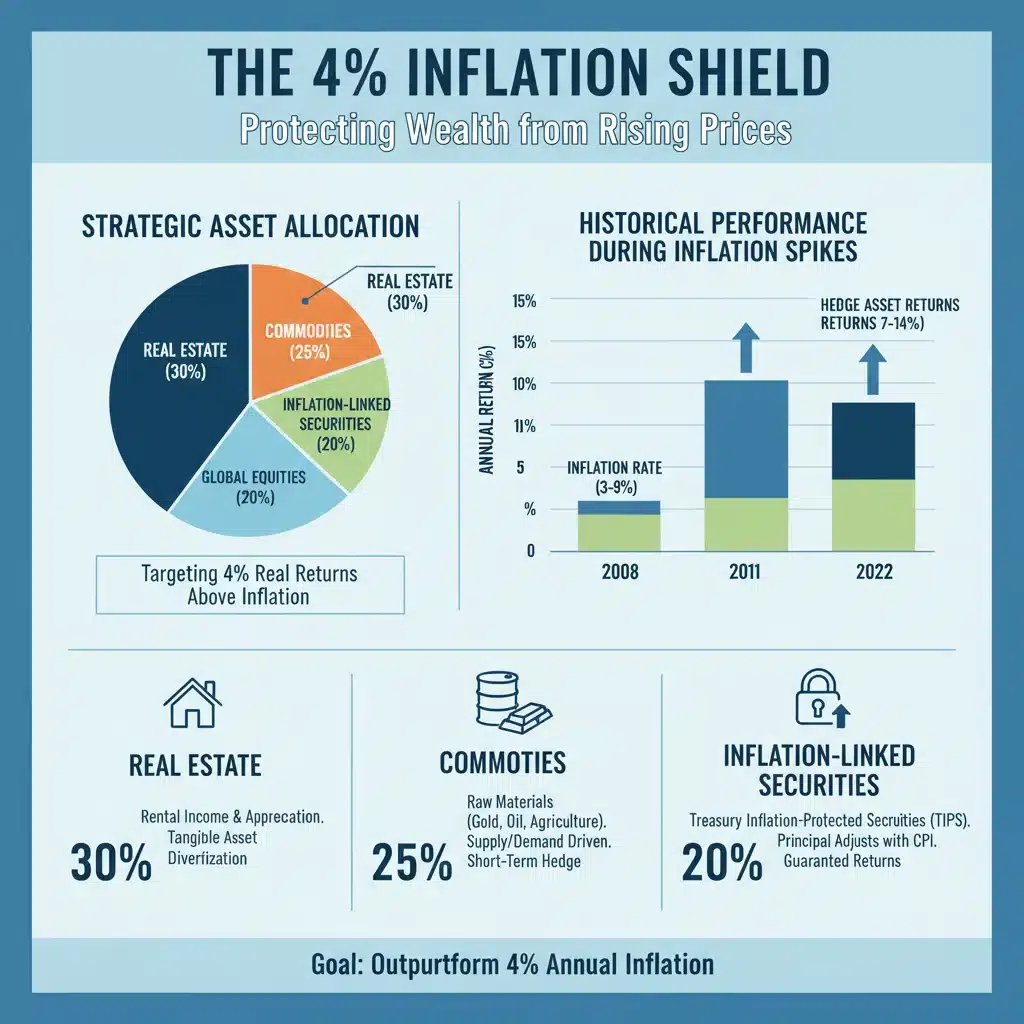

So, what exactly is a ‘4% hedge’ in the context of retirement inflation hedge? It’s not a single investment, but rather a strategic framework designed to ensure your investment portfolio’s real rate of return (after inflation) is sufficient to maintain or increase your purchasing power. The ‘4%’ often refers to a target real return or a benchmark for how much your portfolio needs to outpace inflation to be truly effective. For example, if inflation is 3%, aiming for a 4% real return means your portfolio needs to generate a nominal return of at least 7%. This target provides a concrete goal for your investment strategy, guiding asset allocation and risk management decisions.

Implementing a 4% hedge involves diversifying your portfolio across various asset classes that historically perform well during inflationary periods. It means moving beyond traditional stock and bond allocations and incorporating assets specifically designed to counteract rising prices. This approach recognizes that not all investments react to inflation in the same way. Some assets, like cash, are highly vulnerable, while others, like certain commodities or real estate, can offer significant protection.

The core principle behind a successful retirement inflation hedge is to build a portfolio that is resilient to economic fluctuations, especially those driven by inflation. This requires a dynamic strategy, regularly reviewed and adjusted to prevailing economic conditions. It’s about anticipating challenges and positioning your assets to not just survive, but thrive, in an inflationary environment.

Key Strategies for Building an Effective Retirement Inflation Hedge

1. Inflation-Protected Securities (TIPS)

Treasury Inflation-Protected Securities (TIPS) are bonds issued by the U.S. Treasury that are indexed to inflation. Their principal value adjusts with the Consumer Price Index (CPI), meaning both the principal and interest payments increase with inflation and decrease with deflation. This direct link to inflation makes TIPS one of the most straightforward and effective tools for a retirement inflation hedge. They offer a guaranteed real rate of return, protecting your capital from erosion due to rising prices. While their nominal returns might sometimes be lower than other investments during periods of low inflation, their primary value lies in their ability to preserve purchasing power when inflation is high.

2. Real Estate and REITs

Real estate has long been considered a powerful inflation hedge. Property values and rents tend to rise with inflation, providing a natural shield against the diminishing value of money. Investing directly in physical property, such as rental homes or commercial spaces, can offer both rental income and capital appreciation. For those who prefer a more liquid and diversified approach, Real Estate Investment Trusts (REITs) are an excellent option. REITs are companies that own, operate, or finance income-producing real estate. They trade on major stock exchanges like stocks and are required to distribute a significant portion of their taxable income to shareholders annually, often providing attractive dividend yields that can keep pace with inflation.

3. Commodities and Natural Resources

Commodities, such as oil, natural gas, precious metals (gold, silver), and agricultural products, often perform well during inflationary periods. As the cost of goods and services rises, so too does the price of the raw materials used to produce them. Gold, in particular, has a long history as a store of value and an inflation hedge, often appreciating when confidence in fiat currencies wanes. Investing in commodities can be done through direct purchases, futures contracts, or more commonly, through Exchange Traded Funds (ETFs) that track commodity indices. Natural resource companies (e.g., mining, energy, timber) also tend to benefit from rising commodity prices, making their stocks another potential component of your retirement inflation hedge strategy.

4. Dividend-Paying Stocks and Value Stocks

While not all stocks are equal in their ability to hedge against inflation, certain types can be effective. Companies with strong pricing power – those that can pass on increased costs to consumers without significantly impacting demand – tend to fare better. Dividend-paying stocks, especially those from established companies with a history of increasing dividends, can provide a growing income stream that helps offset inflation. Value stocks, often characterized by strong fundamentals and lower price-to-earnings ratios, can also be resilient. Growth stocks, while appealing, can sometimes be more vulnerable to inflation as their future earnings are discounted at higher rates.

5. Floating-Rate Bonds and Bank Loans

Unlike traditional fixed-rate bonds, whose value can decline when interest rates rise (often a response to inflation), floating-rate bonds and bank loans have interest payments that adjust periodically based on a benchmark rate (like LIBOR or SOFR). This means their yields increase as interest rates rise, providing a natural hedge against inflation. These instruments offer a way to generate income that adapts to changing economic conditions, protecting your income stream’s purchasing power.

6. Annuities with Inflation Riders

For those seeking guaranteed income in retirement, certain annuities can offer inflation protection. While standard fixed annuities provide a predictable income stream, their purchasing power can be eroded by inflation. However, some annuities offer inflation riders or cost-of-living adjustments (COLAs) that increase your payments over time. This ensures that your annuity income maintains its value relative to rising costs, providing a crucial layer of financial security in your later years. It’s important to carefully review the terms and costs associated with these riders, as they can impact the initial payout.

Crafting Your 2026 Retirement Inflation-Protected Portfolio

Building a robust retirement inflation hedge portfolio for 2026 requires a personalized approach. There’s no one-size-fits-all solution, as your risk tolerance, time horizon, and current financial situation will dictate the optimal mix of assets. However, some general principles apply:

- Diversification is Key: Don’t put all your eggs in one basket. A diversified portfolio across various asset classes (stocks, bonds, real estate, commodities, TIPS) is crucial for mitigating risk and capitalizing on different market conditions.

- Long-Term Perspective: Inflation hedging is a long-term strategy. Short-term market fluctuations shouldn’t deter you from your overall objective of preserving purchasing power over decades.

- Regular Review and Rebalancing: Economic conditions change, and so should your portfolio. Regularly review your asset allocation (at least annually) and rebalance as needed to ensure it aligns with your inflation protection goals and risk tolerance.

- Understand the Costs: Every investment comes with fees and expenses. Be mindful of these, as high costs can eat into your returns and diminish the effectiveness of your hedge.

- Consult a Financial Advisor: A qualified financial advisor can help you assess your individual situation, understand the complexities of inflation hedging, and construct a personalized portfolio strategy tailored to your 2026 retirement goals.

The Role of a 4% Withdrawal Rate in an Inflationary Environment

The ‘4% rule’ is a common guideline for retirement withdrawals, suggesting that retirees can safely withdraw 4% of their initial portfolio value (adjusted for inflation each year) without running out of money. In an inflationary environment, adhering to this rule becomes even more critical, and having a strong retirement inflation hedge in place supports its viability. If your portfolio isn’t growing faster than inflation, a 4% withdrawal rate could deplete your savings prematurely. By actively hedging against inflation, you increase the likelihood that your portfolio can sustain these inflation-adjusted withdrawals, ensuring your income lasts throughout your retirement.

Consider the interplay between your investment returns, inflation, and withdrawal rate. If inflation averages 3% and your portfolio yields a nominal return of 7% (a 4% real return), you have a healthy buffer. However, if your portfolio only yields 5% (a 2% real return), a 4% withdrawal rate is unsustainable in the long run. This underscores the importance of not just growing your money, but growing it in real terms, above and beyond the rate of inflation.

Beyond Investments: Other Considerations for Your 2026 Retirement

While investment strategies form the core of a retirement inflation hedge, other aspects of your financial planning also play a significant role in safeguarding your purchasing power:

Healthcare Costs

Healthcare is often one of the largest and most rapidly inflating expenses in retirement. Planning for these costs is crucial. Consider Health Savings Accounts (HSAs) if eligible, as they offer a triple tax advantage (tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses). Additionally, research long-term care insurance options and understand Medicare coverage gaps to avoid unexpected financial burdens.

Part-Time Work or ‘Encore Careers’

Many retirees choose to work part-time, not just for supplemental income, but also for intellectual stimulation and social engagement. Even a modest part-time income can significantly reduce the pressure on your investment portfolio, especially during periods of high inflation or market downturns. This provides an additional layer of financial security and flexibility.

Debt Management

Entering retirement debt-free or with minimal debt is a powerful inflation hedge in itself. Interest rates can rise with inflation, making variable-rate debt more expensive. Eliminating mortgage payments, credit card debt, and other liabilities reduces your fixed expenses, freeing up more of your retirement income for discretionary spending and protecting you from rising interest costs.

Social Security Optimization

Social Security benefits are inflation-adjusted through Cost-of-Living Adjustments (COLAs). While not always perfectly matching inflation, they provide a valuable base of inflation-protected income. Maximizing your Social Security benefits by delaying claiming until your Full Retirement Age or even age 70 can significantly increase your monthly payout and thus your inflation-adjusted income throughout retirement. This is a simple yet effective way to enhance your retirement inflation hedge.

Monitoring Economic Indicators for Your Retirement Inflation Hedge

Staying informed about economic indicators is vital for effective inflation hedging. Key metrics to watch include:

- Consumer Price Index (CPI): The most common measure of inflation, tracking the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

- Producer Price Index (PPI): Measures the average change over time in the selling prices received by domestic producers for their output. It can be an early indicator of future consumer inflation.

- Federal Reserve Interest Rate Decisions: The Federal Reserve’s monetary policy, particularly interest rate adjustments, directly impacts inflation and the performance of various asset classes.

- Commodity Prices: Trends in the prices of oil, gold, and other raw materials can signal inflationary pressures.

- Wage Growth: Strong wage growth can contribute to inflation as businesses pass on higher labor costs to consumers.

By regularly monitoring these indicators, you can make informed decisions about adjusting your retirement inflation hedge strategy, ensuring your portfolio remains responsive to the prevailing economic climate.

Conclusion: Securing Your Financial Future by 2026 and Beyond

The journey towards a secure and comfortable retirement is fraught with various challenges, and inflation stands out as one of the most insidious. As we approach 2026, the need to actively protect your retirement savings from the erosion of purchasing power becomes increasingly urgent. By understanding the mechanisms of inflation and implementing a strategic retirement inflation hedge, particularly one targeting a 4% real return, you can significantly enhance your financial security.

This involves a thoughtful allocation of assets to inflation-resistant investments like TIPS, real estate, commodities, and carefully selected stocks. Furthermore, integrating sound financial planning practices beyond just investments – such as managing healthcare costs, optimizing Social Security, and minimizing debt – creates a holistic defense against inflationary pressures. Remember, your retirement isn’t just about accumulating a large sum of money; it’s about ensuring that money retains its value and can provide the lifestyle you envision. Proactive planning and a robust retirement inflation hedge are your best allies in achieving that goal, allowing you to face your golden years with confidence and peace of mind.